As property prices continue to rise, many investors have considered the option to purchase an investment property with a friend, family member or business partner.

Co-owning property has the immediate benefit of increasing an investor’s purchasing power while reducing the burden of corresponding expenses. However, many investors who co-own property and in particular, those considering co-ownership, are unaware that purchasing an investment property with another party can substantially increase the deductions that can be claimed due to the wear and tear of the items contained in the property.

To ensure that depreciation deductions are maximised, a specialist Quantity Surveyor should be consulted to provide a depreciation schedule based on each owner’s percentage of ownership for each asset. Often investors do not seek adequate professional advice and this can lead to depreciation deductions being claimed incorrectly and in some cases not claimed at all.

It’s not uncommon for co-owners to make the mistake of calculating depreciation first and then splitting the deductions based on the ownership percentage. However, legislation allows co-owners to split an asset’s value by ownership percentage first, potentially qualifying them for higher depreciation deductions. As a result co-owners are able to increase their deductions substantially by writing off plant and equipment items far sooner using methods such as low-value pooling and immediate write-off.

Low-value pooling

Low-value pooling is a method of depreciation which allows an investor with an ownership interest in an asset of less than $1,000 in value to claim deductions at an accelerated rate of 18.75% in the year of purchase and 37.5% each year afterwards. As each investor’s ownership interest may qualify for the low-value pool, co-ownership expands the number of items that can be claimed at this higher rate of depreciation.

Immediate write-off

Legislation allows property investors to claim an immediate write-off for assets with an opening value of $300 or less. In a situation where ownership is split between one or more parties, the rule allows investors to claim an immediate write-off to items where an owner’s interest in the asset is below $300.

CASE STUDY

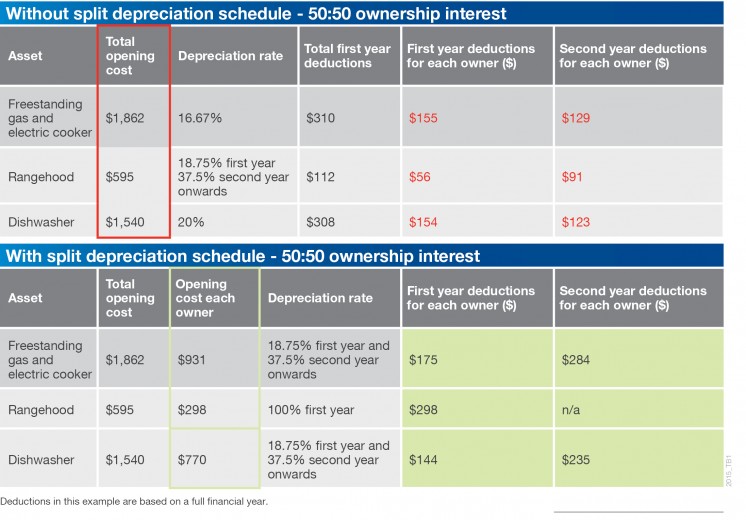

Let’s take a look at an example of how the immediate write-off and low-value pooling rules apply to some of the depreciable assets generally found in the kitchen of every investment property.

The table below demonstrates the impact that a split depreciation schedule will have on qualifying the owners to increased deductions sooner when compared to a situation where deductions are claimed without performing the split allocation first.

By obtaining a split depreciation schedule, the first year claim for each owner will improve from $365 to $617 and the second year claim will improve from $343 to $519.

The freestanding gas and electric cooker purchased for $1,862 and the dishwasher purchased for $1,540 are able to be depreciated using the low-value pool, greatly increasing the value of deductions.

Using a split schedule also allows the owners to claim an immediate write-off for the range hood, as the 50% ownership percentage split will further reduce the opening cost of this asset to $298 for each owner (less than the $300 threshold set by the ATO).

The increase in deductions that a split depreciation schedule provides are made even more significant when all of the assets typically found in an investment property are included.

A split depreciation schedule is available in any scenario where an investment property is co-owned, whether it is for a husband and wife, friends or business partners.

The deductions using a split schedule can also be calculated based on any number of investors and the percentage of ownership each individual has in the assets, whether it’s for two owners at 60:40 or 1:99, or even four owners at 70:15:10:5.

For owners with lower percentages of ownership, the low-value pool and immediate write-off will apply to more assets, increasing deductions earlier. This is particularly important for investors to understand when entering into a co-ownership agreement and at the time of purchase. For example, a husband and wife might choose to align their percentage of ownership so that the higher income earner holds the greater portion of interest in the assets and therefore that person will be able to claim a higher portion of the deductions at tax time.

It’s important to note however that once an investor has requested a split depreciation schedule, they cannot change their interest in the assets within the property down the track. Depreciation must always be claimed at the percentage of ownership split that is outlined on the original schedule from settlement.

Article provided by BMT Tax Depreciation.